Not just the Fed: why we've had 0% rates for so long

The structural forces keeping interest rates low

While most people believe that central banks alone are responsible for keeping interest rates low for the previous decade, I’d like to look at some of the larger structural forces that also have an effect on rates. Certainly central banks the world over play a role in ZIRP (zero interest rate policy) but we cannot ignore the other causes either.

Reading through Michael Howell’s book Capital Wars (review coming soon) I came across an especially interesting paragraph.

Rates of return on capital are ultimately equalised across economies by capital mobility and the reshuffling of investments. Secular movements in real interest rates combine these changes in saving and investment behavior with fluctuations in the safety and liquidity properties of safe assets, such as Treasury instruments. We argue that both falling industrial profitability and the associated structural shortage of safe assets are key factors behind the long downward slide in World interest rates.

And now take a look at this chart…

This graph suggests that while there may be short-term volatility, there is a long-term trend towards lower returns on industrial capital. I.e lower returns on capital invested in the real economy, hence a preference for safe investments. It’s not the first time that I’ve come across this idea, however, it’s only now that I’m putting the puzzle together. The way I see it, to get a clear idea of what’s going on with interest rates we have to look at how life has changed in the last 150 years.

Then vs now: a tale of two growths

A woman is born to lower middle class parents in 1880, what is her life like? She makes her own clothes, rides a horse or takes a horse drawn carriage. At night she lights her house with candles or later on kerosene, there is no electricity until the turn of the century. Without running water the woman must carry hundreds of gallons of water in and out of the house every week. She might go years without traveling more than fifteen or twenty miles from her home, if that.

If this woman lives to be 90 the year will be 1970. The same woman cooks on a gas stove, uses indoor plumbing, buys her clothes from a store, rides in a car and (if she can afford it) flies across the country in an airplane. Truly, in the 90 years she has been alive the woman’s life has radically changed for the better. That’s real growth and innovation!

Throughout that period of rapid advancement investors were presented with the opportunity to fund the development of the real economy and earn an attractive return on their capital. With all of that innovation taking place, you’d be crazy to not put your dollars to work with entrepreneurs and businesses that are, quite literally, changing the world.

Unfortunately, real growth has been on the decline for decades (see here). All of the “easy” innovations, like switching from a horse to a car, have already been accomplished. Innovation today, such as it exists, is Apple adding another camera to their phone. Marginally better definition on our televisions, unnecessarily exotic materials in our sneakers, lighter weight clothing, etc. All of this is fine and good, but it’s not life changing. We haven’t cured cancer*, mastered gravity or solved fission energy at scale.

*In fact, average lifespans in America are actually going down!

Zero interest rates

Returning to that graph from above, we can see how investor preferences affect interest rates. As there are fewer good opportunities to earn a high ROI from businesses building products, investors will allocate more to safe assets like government bonds. If enough people/banks/institutions do so, this can meaningfully drive down yields resulting in lower interest rates in the economy.

Furthermore, as I detailed in my article How the Eurodollar system works, the massive Eurodollar network with an estimated size of between $50 and $150 trillion is a collateral based lending system. While it’s possible to use private sector assets to secure a loan, the gold standard in collateral are government bonds, particularly US Treasuries. The size of the Eurodollar lending market guarantees a constant demand for Treasuries, which is another structural force putting downward pressure on rates.

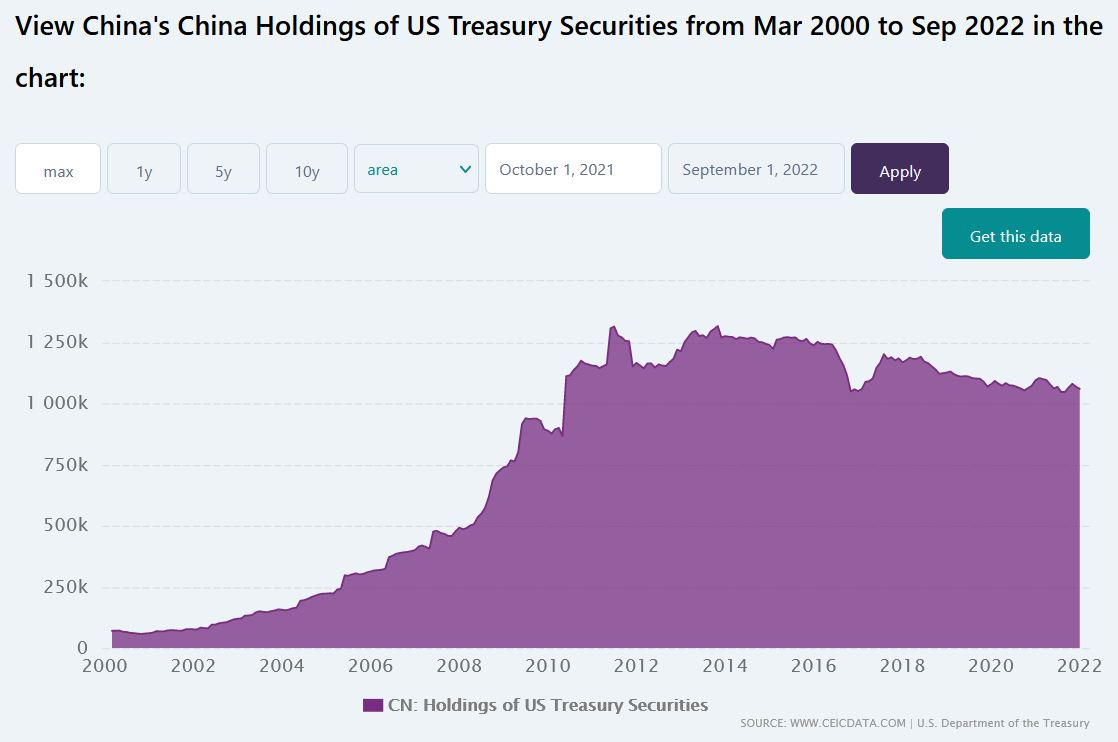

Finally, foreign buyers love (*historically* have loved) Treasuries. In 2013 Chinese holdings of US Treasuries peaked at about $1.3 trillion. Recently China has divested itself of some of these bonds, but they still own about $1 trillion worth. At one point Russia owned about $100 billion of Treasuries, but they’ve dumped most of that paper/had it stolen.

Being a small island nation, Japan only holds a paltry $1.2 trillion in Treasuries, or $9,500 worth of USTs for each Japanese man, woman & child. Dozens of other countries have also invested in American government debt and the recycling of dollars into Treasuries is yet another factor driving down interest rates.

Implications

I just detailed the structural forces outside of anyone’s control that have forced us into a low interest rate regime. Of the three factors I listed, I would speculate that a lack of innovation in our physical world is the number one force keeping rates down. It is nobody’s fault - not even the Fed’s - that real growth is harder to achieve in the modern age.

While central banks can manipulate rates short-term rates (see my article explaining why the Fed can’t control long-term rates), the larger forces operating in our current financial system suggest that there will always be constant downward pressure on interest rates. The implication is that while there will be rate spikes as inflation waxes and wanes, rates could keep surprising to the downside.

I would speculate that there’s even a possibility that we won’t get permanently higher rates until we discover new technologies that people are excited to invest in. If/once a new generation of tech comes online, investors will get greedy again. They’ll sell their bonds yielding whatever-low-percent and invest in companies and entrepreneurs promising big returns on invested capital. A new cycle of innovation will take place, rates will remain high and let’s hope it happens sooner rather than later.

Every Sunday I publish a recap of all the best finance articles and podcast episodes I’ve found thought-provoking. Here’s the latest edition.

If you’d like to get this free newsletter straight to your inbox just enter your email below 👇

Great article. Reminds of of Jeff Booth’s great book the “price of Tommorrow”

would you agree with the following? Is this a fair summary?

Because of the lack innovation, people have instead invested in gov bonds because it is the safest borrower. buying treasuries in the open market pushes yields down. because the US gov is the safest debtor, this becomes the "free market" interest rate.