The Treasury is going to buy... Treasuries?

Joseph Wang thinks so. Here's what you need to know

Joseph Wang just let loose a new post which I found interesting. You should definitely read the original piece, it’s not that long. I just want to write a brief summary, and also provide a few explanations of what’s going on here.

The argument

Mr. Joseph argues that the Treasury might buy treasuries to help market liquidity. The Treasury could make those purchases using reserves (draw down the TGA), or they could issue new debt to buy the old debt. To what end?

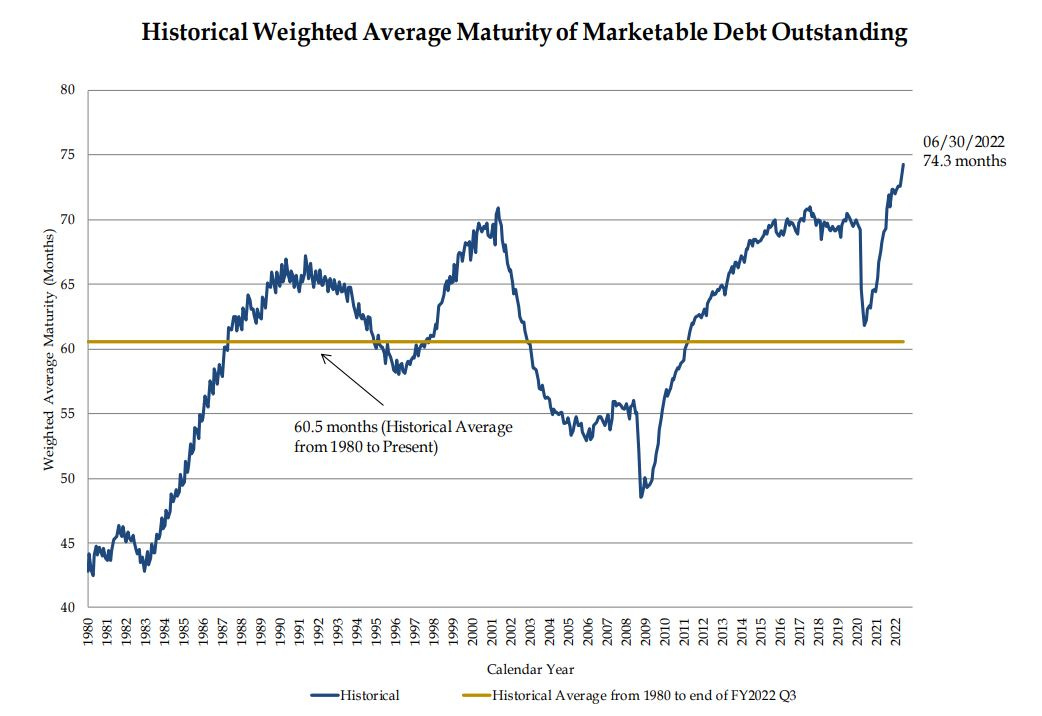

Short term treasury bills are the most desirable financial asset. The market must have its t-bills, and when there’s not enough in the system bad things tend to happen. So Treasury could buy back longer maturity notes and bonds, and issue more t-bills to help lubricate the economic machinery. Check out this picture below and you can see that the average duration of treasuries in the marketplace is unusually high. Not ideal.

Joseph also makes the point that if markets are holding more t-bills than bonds, interest rate sensitivity is decreased. That makes sense, although I’m not entirely sure what the implications are? I’ll leave that up to you to decide.

Coupon Treasuries?

Joseph writes, “In theory, the Treasury would be able to act in a similar role by issuing bills and using the proceeds to buy coupon Treasuries.”

It took me a moment to puzzle out the phrase “coupon treasuries,” but I think I’ve got it now. Coupon treasuries is a linguistically interesting way of referring to longer duration notes and bonds. These assets, which take years or decades to mature, pay a coupon to investors. T-bills are different.

Instead of issuing a coupon for t-bills, Treasury sells them at a discount. For example, let’s say Treasury auctions off some bills and the yield is 1%. The investor pays $0.99 on the dollar for the bill. At maturity the investor receives $1, thus the 1% yield.

I’m not sure when baked-in-yields stops being a thing and coupons take over. Maybe on a two year note? At any rate, coupon treasuries is a term referring to anything that’s not a bill.

Edit to this post…

After further research, I discovered that my initial ideas weren’t so brilliant. In retrospect I think Joseph may have been saying that Treasury could buy regular coupon treasuries, as opposed to zero coupon treasuries which are apparently a thing. You learn something new everyday.