Why Alex Gurevich thinks we're headed for a deflationary depression

Is this how inflation dies?

Alex Gurevich has hypothesized that the concern isn’t spiraling inflation, the real monetary gremlin is a deflationary depression. This intrigues me. When I hear an intellectually capable person argue a viewpoint that goes counter to the mainstream narrative, I want to know why they’re engaged in heresy and whether they might be correct.

My intention with this article isn’t to endorse Alex’s theory or to convince you that he’s right. Rather, I want to explain why Alex is making such a bold claim and what evidence exists to support his argument. Figuring out the rest is up to you, dear reader.

I’m pulling quotes from two different videos, which I’ll post at the end of this article. I think the MacroVoices interview is the better of the two, if you’re only going to watch one. So without further introduction, here’s why Alex thinks the worst is yet to come.

Monetary policy lag

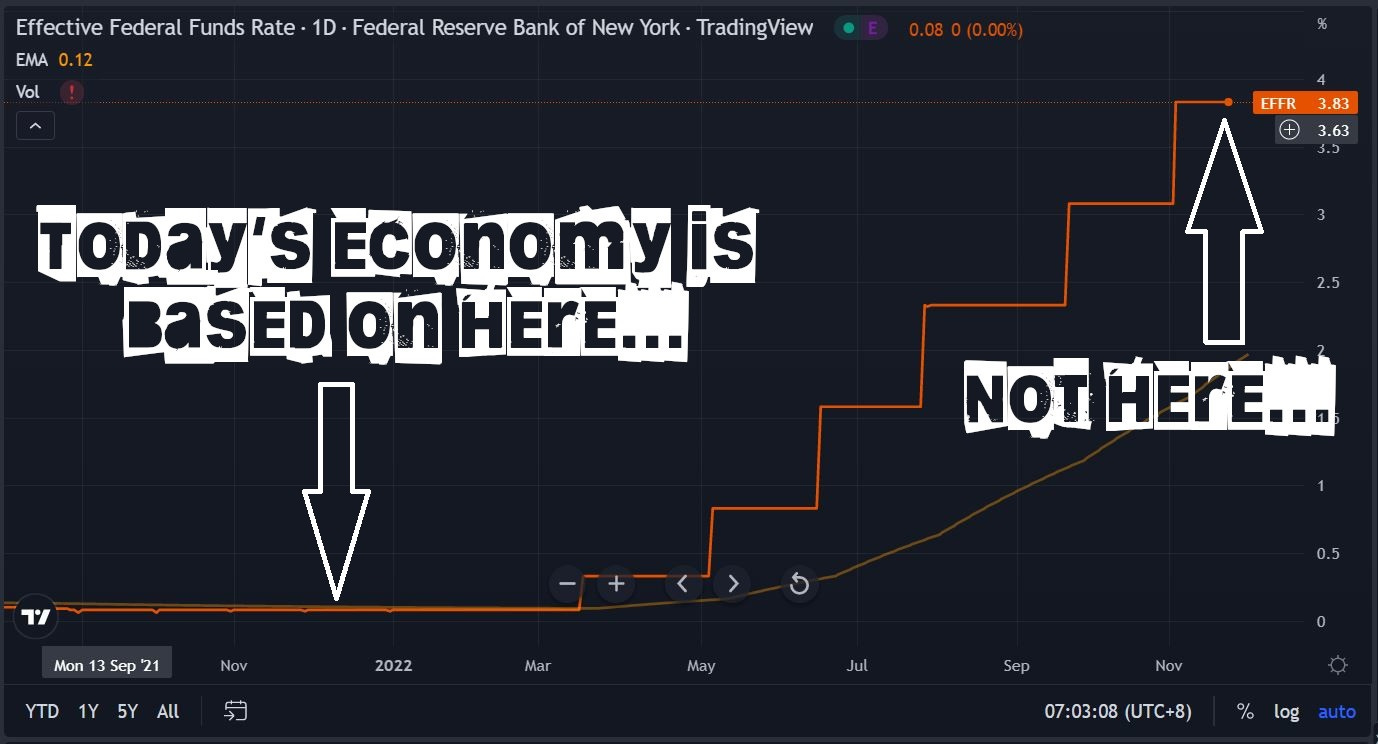

Alex’s key point is that monetary policy operates on a lag. According to Jay Powell himself, the effects of interest rate policy take between one and two years to manifest in the real economy. Higher interest rates blow up tech and crypto first, then the stock market and housing, then the economy. As such, Alex points out that everything that’s happening in the markets right now is the result of policy in 2021.

That marginally lower CPI print that caused the S&P to gap up? That small drop in inflation numbers isn’t because Fed Funds is now at 3.75%, it’s the result of the gradual tightening that started a year ago! The implication is powerful… Our current economic condition is the result of Fed policy and interest rates from last winter. One year ago Fed Funds was at 0%, and we’re already in a not-so-great economic situation. What’s going to happen once 4% interest rates work their way through?

I might caveat this argument, however, by pointing out that not everything operates on a lag. For instance, mortgage rates have risen in lockstep with interest rates, so the housing market is already in a bad way. Little lag there. So perhaps we cannot say that all monetary policy comes with a lag. At any rate, here’s Alex in his own words.

Quote from MacroVoices @ 27:10

I was listening very carefully to Powell during his press conference, and I’m trying to understand: is there something that they know that I don’t? Because my assumption is that they know more than I do. - So let’s go through what he says. He reiterated that the lag from policy are long and variable. This is a very difficult thing to internalize. No matter how many times you repeat that, it’s very difficult to believe that policy does not affect inflation right away. Right away means that the lag of actual inflationary impact is between one and two years. Saying that it’s one year, that’s generous. - Nothing we see about inflation and the job market in 2022 has anything to do with policy in 2022. So the policy changes of 2022 absolutely cannot have any effect yet on inflation or the job market.

The Fed is perpetually behind the curve

The Fed is well-known for crafting policy based on lagging indicators. For instance, a decrease in the price of housing might not show up in the CPI for six months to a year. By the time the Fed sees the data proving that the housing market is slowing down, the actual market might already be in a severe correction.

The problem with lagging indicators is that you end up with a situation like what we have today. The Fed is raising rates into a slowdown! Assuming that we are headed into a recession, the Fed's maniacal tightening policy is like kicking a man in the kidneys when he’s already crawling through the mud and bleeding out of the ears. It’s just poor form.

Quote from MacroVoices @ 32:08

By the time they [the Fed] see inflation coming down, they will see that as a lagging indicator. They will already be one or two years behind the curve. They will have been tightening for two years, in a period of time in which they should have been easing. By the way, I believe that the current correct policy would be easing, but they’re still tightening because they’re looking at the lagging indicators.

Globally coordinated tightening

For the last twenty odd years, China’s continued growth has been a major force in pulling other countries out of their economic funks. China’s economy has averaged in the ballpark of 8% annual GDP growth. Combined with the country’s massive population, that growth was enough to at least partially pave over economic contractions in the US or Europe. China’s climb up the developmental ladder is why Australia, as a commodity exporter, hasn’t had a recession since the bronze age.

This time is different. China’s growth was slowing before Covid, and we’ve all seen what’s happening with the zealous zero Covid policies. Depending on how conspiratorial you want to get, the CCP is either waging war against germs, or conditioning their citizens for a brutal authoritarian future, all hail the supreme leader. Whatever the real reasons for the lockdowns the effect is the same: economic suicide. China is in the process of blowing up their magical prosperity machine. There will be no Chinese growth to save the world from a protracted recession this time around.

Quote from Jay Martin @ 22:00

It’s a matter of degree. I just think the conditions are higher for a coordinated recession because in past recessions China was the big growth engine for the world and that’s kind of gone away now. China has huge overhangs of over-priced real estate and other problems as well. Europe is struggling with the energy crisis. Europe might be able to pull itself out with military and infrastructure investment, so Europe has outs, as opposed to China which has less outs. Paradoxically, the US is doing better for now, but it has no easy way to get out of this situation.

The videos

Closing thoughts

The Tl;Dr on Alex’s argument: the economy is weak and rather than support it, the Fed is shanking it in the heart with a rusty bayonet. Furthermore, because the Fed is blinded by backward looking indicators, it will not change policy until the the United States is already in a (deep) recession. The lagging effect of monetary policy means that even once the Fed pivots, the economy will remain in poor shape for a while longer.

Implication for asset allocation? In all honesty, my allocation strategy probably won’t change that much. If there is one silver lining to this economic abyss, it’s that assets are likely to get very cheap. I will continue to buy energy stocks and gold miners, fully prepared to weather tough drawdowns in the coming quarters.

The one (deflationary depression) doesn‘t excludebthe other (inflationary crack up), in fact they are both different sides of the same coin. Mises (and Rothbard) both point to the difficulty in knowing whether the deflationary depression will be preceded by an (hyper) inflationary spike in asset prices and wages or not. In the end it doesn‘t matter: the resulting liquidation of unsustainable debt levels and the wholesale destruction of demand will result in a depression. The only real question is whether it will be allowed to sort itself out quickly (1921) or be so chronically interfered with by the same people who caused it in the first place that it takes a decade or two to play out.